Younger millennials have it the worst with this auto loan trend

Outside of buying a home, a car is the most expensive purchase most Americans will make in their lifetimes. Unfortunately, one particular generational group is seeing a larger increase in those payments.

Car buyers are understandably very price sensitive.

President Donald Trump’s tariffs, which on Friday, Feb. 20, the Supreme Court ruled were unlawful, threatened to add thousands to price tags, so car buyers flocked to dealerships early last year. Looking to capitalize on this added interest, carmakers rolled out incentives to get potential buyers through the door.

Retail consumers spent $620 billion on new vehicles in 2025, according to Automotive World, citing J.D. Power data, a nearly 6% increase from the previous year.

“Affordability pressures remain significant, with monthly finance payments reaching a new record for the month of December at $776,” said Thomas King, president of OEM solutions at J.D. Power.

While all Americans are feeling the pinch from these higher prices, younger millennials are paying more than other age groups, according to Bank of America.

Younger millennials see the biggest increase in monthly car payments

Consumers paid an average transaction price of $49,191 per vehicle in January, a nearly 2% increase from a year ago, according to Kelley Blue Book, but according to new research from Bank of America, the price increases weren’t distributed evenly.

While tariffs helped goose auto sales during the first half of the year, a pronounced slowdown occurred in the second half.

Related: New car buyers are resorting to a risky trend

Carmakers sold 15.9 million vehicles last year, down from 16.8 million the year prior, Cox Automotive sales data show. Bank of America says that decline was driven by high prices.

“Auto sales have been tapping the brakes over the last few years, and in our view, affordability pressures are a key reason why,” the firm said in a recent note.

But customer data also indicate that younger millennials (ages 30-36) have seen their bills climb more compared to other age groups. Younger millennials’ monthly car payments rose by nearly 60% since 2019. Older millennials and Gen Z have also seen big increases, but they’re just above 40%.

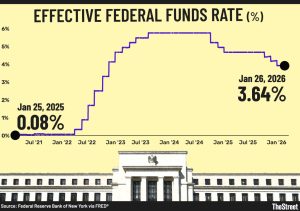

“Why is affordability weighing so heavily on consumers now? Throughout the 2020s, car prices and motor vehicle insurance have climbed significantly. At the same time, Federal Reserve rate hikes have made car loans more expensive,” Bank of America said.

“Taken together, these three factors have raised the overall cost of purchasing and owning a car, which has likely impacted younger generations the most — as they may be building families and scaling up their vehicles.”

More Americans take out 84-month car loan terms

Car manufacturers relied on incentive pricing to help address consumer affordability concerns in 2025.

Ford rode dealer incentives, combined with consumer anxiety about tariffs, to become the top-selling brand in the U.S. during the year’s first half. Ford said total sales in the second quarter rose at a rate seven times that of the overall auto industry.

Related: $50,000 average new car prices are here to stay

“Automakers are providing healthy incentives to keep sales flowing. Prices are trending higher, but just as we are seeing in the broader retail markets, there’s sufficient demand and generous incentives out there, and that’s driving the market,” said Cox Automotive Executive Analyst Erin Keating earlier this year.

However, as the year progressed and the tariff situation became clearer, incentive spending declined.

The average manufacturer’s incentive spend per vehicle in December was $3,433, representing just a $77 increase from the same period a year ago. Incentive spending on average represents about 6.5% of a vehicle’s MSRP, a 0.1% increase.

To make up the gap, more customers are resorting to extended 84-month loan terms, which accounted for 10.1% of financed sales in December, according to J.D. Power.

That’s the second-highest level on record for the month after 2021.

U.S. car buyers are spending too much on driving

Most financial experts recommend spending no more than 15% of your monthly income on a vehicle.

In addition to capping your car payments at about 15% of your monthly take-home pay, financial experts also recommend that shoppers aim for a 20% down payment, a 36- to 48-month loan term, and expenses (including insurance) at between 8% and 10% of your gross monthly income.

According to a MarketWatch Guides survey, about 10% of drivers say they spend 30% of their monthly income on driving, while another 12% said they “found themselves living paycheck to paycheck due to the financial strain of their cars.”

Nearly half of U.S. drivers cite car expenses as the reason they can’t save any money, and the average American spends about 20% of their monthly income on auto loans, fuel, insurance, and maintenance.

A Bank of America survey from this summer found that among households with a monthly car payment, 20% have a payment over $1,000.

Baby boomers, Gen X, and older millennials all saw decreases in the percentage of car owners paying more than $2,000 a month for their vehicles in the past few months.

Gen Z and younger millennials saw an increase in those paying more than that amount.

Bank of America also observed an increase in $2,000-per-month auto bills among people making less than $50,000 and making between between $50,00 and $100,000. Meanwhile, that type of spending decreased among people making more than $100,000.

“Bank of America payments data shows that overall median car payments are already more than 30% higher than the 2019 average and have now outpaced both new and used car prices, possibly as there is a push towards more expensive cars,” analysts Taylor Bowley and David Tinsley wrote.

Related: Tesla proves it truly is a tech (not car) company with latest move